Understanding Curve: a beginner’s guide and review

Extremely efficient stablecoin trading and supplemental fee income for liquidity providers, from seven pools in 2020 to hundreds today.If you've watched stablecoin swaps slip on general-purpose DEXs and wondered how Curve keeps slippage near zero, this article has the answer. You'll learn how the StableSwap algorithm prices like-pegged assets, how locking $CRV into veCRV boosts LP rewards up to 2.5x and drives governance, and how Curve survived the 2023 Vyper exploit and its founder's 2024 liquidations to remain DeFi's stablecoin backbone.

Curve Finance is one of the most popular projects currently operating within the DeFi space. Having started off with stablecoin swapping functionality with low slippage, Curve has now been integrated into many different nooks and crannies of the DeFi ecosystem.

TL;DR: You can get a summary of this article on its last section

In this article, we will be taking an introductory look at Curve Finance to better understand how this protocol became core infrastructure in the DeFi space. In this analysis of Curve, 5 different sections will be covered, as follows:

- legitimacy

- purpose

- tokenomics

- ecosystem

- summary.

Legitimacy

Curve was originally conceived by Dr. Michael Egorov, a Russian physicist, and entrepreneur who previously cofounded NuCypher, an encryption protocol for big data. NuCypher was seeded with $750,000 from YCombinator in 2016, later raising $15.1 million in two rounds in 2017 and 2018 led by Polychain, with participation from Fenbushi Capital, Compound VC, and others.

Egorov served as NuCypher’s CTO, and while developing the staking mechanism for NuCypher’s NU token studied the concepts of liquid staking and bonding curves. Egorov developed a low-slippage trading algorithm that could run within an Ethereum smart contract and started working towards Curve, while NuCypher went on to decentralize from genesis through its token generation event (TGE) in the form of the WorkLock, a novel stake-and-work-to-earn approach to issuing its first tokens.

Curve was launched in January 2020 and started grabbing headlines immediately due to its composability, or design fit with other permissionless components of the DeFi ecosystem. However, the biggest shock to the Crypto-Verse came with the surprising events of August 2020 when Curve decided to launch its governance token, $CRV . Curve community user 0xc4ad, a newly created account, unilaterally spent around $8k and deployed the open-source token and the CurveDAO contracts on the Ethereum mainnet, with the Curve team allegedly not involved and only learning about the feat through the user’s Twitter announcement and later officializing the launch after a few hours of reviewing the deployment. Definitely, one of the most controversial DeFi launches ever.

Just 4 days after that episode, Curve would become one of the largest DeFi protocols, the third ever to receive over $1B in total value locked (TVL).

Purpose

Curve is based on the StableSwap Whitepaper made by Egorov in November 2019. The issue Curve is meant to solve is the liquidity and price stability issues of stablecoins, particularly centralized finance (CeFi) protocols like $USDT and $USDC which have a central point of failure. Curve effortlessly automates the process of providing much-needed liquidity to stablecoins in an environment that is completely free of middlemen.

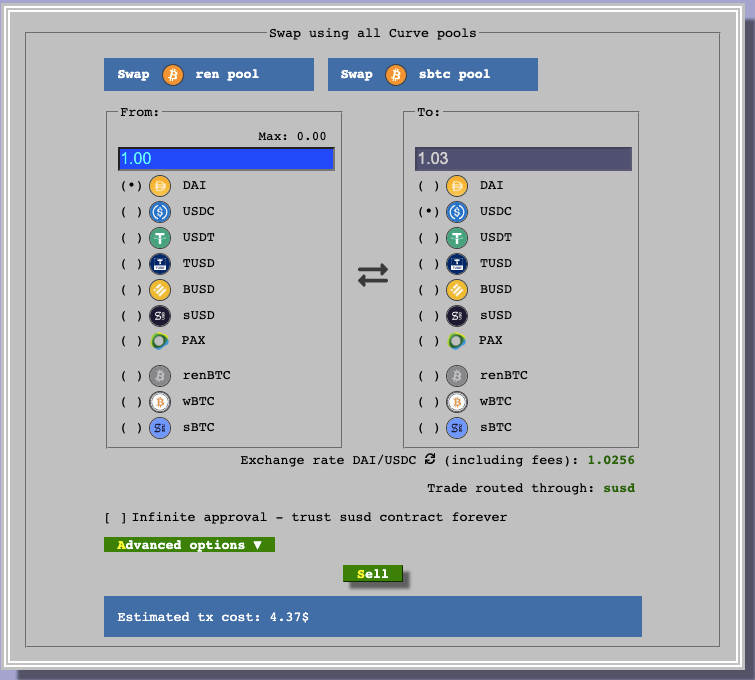

At launch, Curve supported seven stablecoins pegged to the US dollar ($DAI , $USDC , $USDT , $TUSD , $BUSD , $sUSD, $PAX ) and three coins pegged to $BTC ($renBTC, $wBTC, $sBTC). Today it runs hundreds of pools across Ethereum and a dozen other chains, and several of those early assets ($BUSD , $PAX , $renBTC, $sBTC) have since been retired. It is available as a Curve web app. Getting started on trading is simple and efficient, with support currently built-in for a variety of crypto wallets.

If you’re looking to get started on Curve, I would highly recommend that you connect a Metamask wallet and play around the interface.

Tokenomics

Curve claims to offer quick and secure trading with the lowest possible slippage, which is the difference between the quoted price and the execution price of the trade. Curve fees started at 0.04% per transaction on each of its pools, all of which went to liquidity providers (LPs) sans admin fees. As governance changed, the fees did too: they now diverge across pools, and half of them flow to veCRV holders as admin fees.

At the time of this review there were 7 pools in Curve, five for stablecoins,

and 2 for tokenized Bitcoinor Bitcoin -on- Ethereum (also known as $wBTC).

All pools earned yield from trading fees, but on four of the pools,

there was further interest from lending as behind the scenes,

these pools used lending protocols

( Compound ($COMP ) and Yearn ($YFI ) )

to maximize return for the LPs.

For example, the user received either a cToken (for the comp pool) or a yToken

(for the pax, y, and busd pools).

Other pools like susd and sbtc were non-lending pools

but were incentivized by the partnership between Curve and Synthetix

and received rewards in SNX.

The ren pool was a more classic pool with $renBTC and $wBTC.

Both Bitcoin pools depended on the Ren protocol,

which shut down after the FTX collapse in 2022 and took $renBTC with it.

Curve's pool lineup has since grown into the hundreds, spanning stablecoins,

$wBTC, $ETH derivatives, and volatile pairs.

When looking at a pool to invest,

one needs to consider systemic risk and exposure to different assets

and smart contracts.

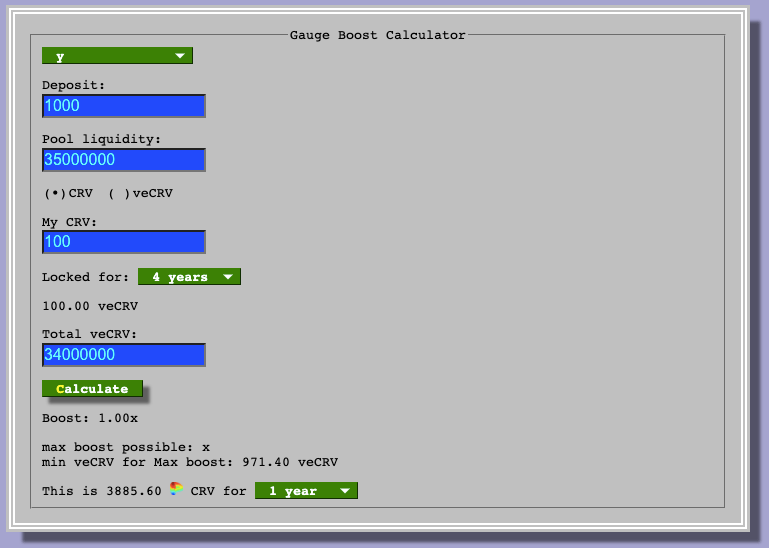

To provide further incentives to liquidity, Curve created a token, $CRV , which launched after the protocol had been live for 8 months. $CRV is a governance token, an increasingly popular primitive in tokenomics models, particularly in the DeFi space. These types of tokens confer both economic and voting rights to their holders, and in many ways could be considered somewhat analogous to equities, even if they are categorized as utility tokens. They allow holders to participate in the “governance” of a protocol, that is, to vote on proposals according to the protocol’s governance rules. Truly decentralized protocols aim to submit all manners of issues to the community to decide. Issues like voting on improvement proposals, admins, grants, incentives, and possibly the voting mechanism itself.

The $CRV token allows users to participate in the Curve DAO,

or decentralized autonomous organization,

which has administered the Curve protocol since 2020.

The DAO wields economic incentives like inflation

and burning via buy-back of $CRV tokens,

which can be earned by staking counterparty LP tokens

(received when providing liquidity to any of Curve pools)

into the Curve DAO minter.

Those

$CRV tokens can be further locked into the voting escrow contract to receive veCRV, which boosts the rate at which $CRV

rewards are received by up to 2.5x and gives “votes” on the Curve DAO.

Keep in mind lockup periods are irreversible

and involve forfeiting the right to sell your $CRV tokens.

The early proposal to introduce an admin fee passed:

veCRV holders now collect half of the trading fees.

$CRV is traded in secondary markets as well. According to CoinMarketCap, $CRV is found with the most volume and liquidity on the following exchanges:

| Exchange | Trading Pairs |

|---|---|

| Binance | $CRV/$USDT, $CRV/$BTC, $CRV/$BNB |

| OKX | $CRV/$USDT, $CRV/$BTC, $CRV/$ETH |

| Uniswap | $CRV/$wETH |

| HTX | $CRV/$USDT, $CRV/$BTC, $CRV/$ETH |

Ecosystem

As with other DEXs, traders constitute the bulk of the user base, while the others within the ecosystem are liquidity providers and developers. Traders pay a nominal fee to swap between different tokens within the exchange, which in turn goes towards liquidity providers. Finally, developers work towards the integration of Curve with third-party projects, such as Yearn Finance ($YFI ) and Synthetix.

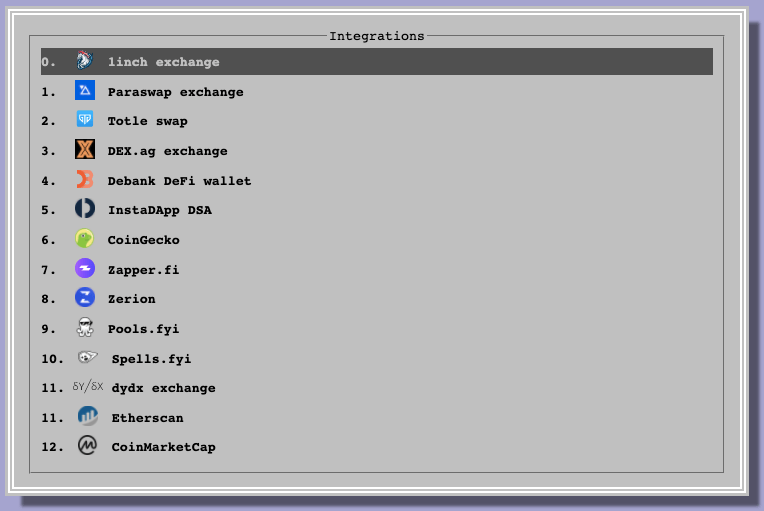

Many integrations have been built for Curve in a very short time. 1inch, Paraswap, Totle, DEX.ag, and DeBank all see the utility in offering affordable stablecoin swaps to their users. This brings more incentives for liquidity, as it creates more volume, which added to existing incentives by Curve itself creates the perfect storm for network effects going forward.

The Curve community is mostly composed of LPs and $CRV holders and is at present very focused on maximizing the benefits of governance for early LPs into Curve.

Curve from 2020 to 2026

The years since this review tested Curve harder than most protocols. In 2023 it launched crvUSD, its own overcollateralized stablecoin with a soft-liquidation mechanism, adding a lending business on top of the DEX.

That same year brought its worst day. On July 30, 2023, a compiler bug in Vyper (the Python-like language Curve’s contracts are written in) enabled reentrancy attacks that drained roughly $50–70M from several pools. Most of the funds were returned or recovered in the weeks that followed, and the DAO voted to reimburse affected LPs for the rest.

The exploit also strained founder Michael Egorov’s personal loans, backed by hundreds of millions of dollars of $CRV ; in June 2024 around $140M of those positions were liquidated and unwound. The protocol absorbed both shocks: pools kept trading, crvUSD held its peg, and Curve remains the default venue for stablecoin liquidity in DeFi.

In Summary

Curve’s focus on stablecoins allows it a degree of protection from the potential volatility that other DEXs are typically exposed to. Its simplicity and speed of development have quickly integrated it into the DeFi ecosystem in general, and in particular, connected it with $YFI via the Curve Y pool, then the largest LP pool in all of DeFi. With decentralized governance, we can expect Curve to keep making DeFi a more reliable place for all involved.

Recommended to Read Next

straight to your inbox